The rapidly evolving landscape of financial technology signifies a crucial shift in 2026. The sector has progressed beyond mere “digitization of banking” into a new epoch of Autonomous Finance.

Presently, fintech engineering encompasses more than monetary transactions; it involves managing an intricate network of Agentic AI, adhering to real-time ISO 20022 data standards, and establishing the requisite infrastructure for instantaneous cross-border settlements.

In this article, we break down the top 06 tech stacks shaping fintech development in 2026 – what each one solves, where it earns its place in a serious financial architecture, and the real-world lessons our teams have learned building with each of them in production.

Key Takeaways

- Stack selection in 2026 demands compliance, throughput, and technical capability; poor choices risk exposure.

- Modern fintech requires architecture to simultaneously support Agentic AI, real-time settlement, and open banking APIs.

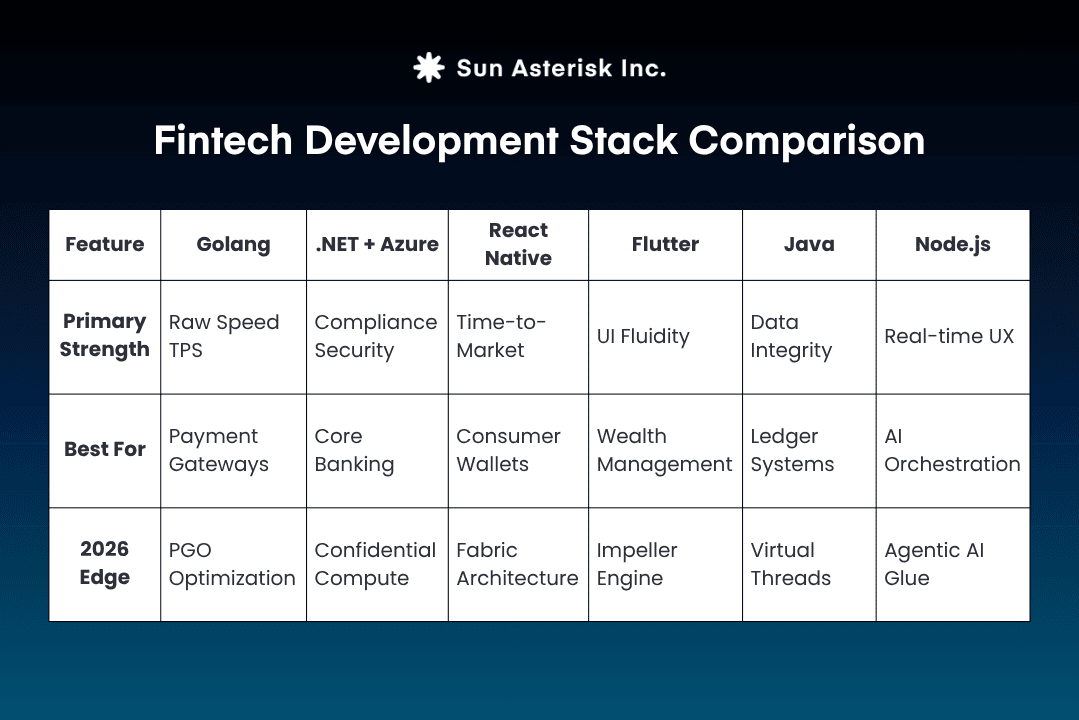

- No single stack dominates: Go is best for throughput, .NET/Azure for regulation/compliance, Flutter/React Native for mobile, Java for enterprise state, and Node.js for real-time/AI orchestration.

- The most robust fintech products use a thoughtful polyglot approach, matching each layer to the optimal stack for its specific constraints.

The Fintech Engineering Reality in 2026

AI has advanced beyond features like chatbots to Agentic AI, which autonomously executes complex, multi-step financial workflows and makes real-time decisions rapidly. Examples include production-scale systems for fraud detection (scoring transactions in under 50ms) and explainable alternative credit models for thin-file borrowers that meet ECOA requirements.

With new regulatory clarity, engineers are increasingly using stablecoins as programmable, 24/7 settlement layers for cross-border payments and treasury operations, replacing slow, costly, weekend-closed legacy infrastructure.

Given the explosion in open banking, financial APIs are prime security targets. Fintech engineering adopts Zero Trust, mTLS, and tokenization to secure the API layer, recognizing that a breach is both a data and a major regulatory problem.

Key Factors to Consider When Choosing a Fintech Tech Stack

Before evaluating any individual stack, teams need clarity on the constraints that should anchor every architecture decision in fintech.

The starting point is always throughput and latency profile. Whether you’re processing 1,000 TPS or 100,000+ fundamentally changes what “good architecture” means, and no amount of horizontal scaling compensates for a wrong foundational choice.

Compliance is non-negotiable and it must be provable. PCI-DSS, PSD2, MiCA, and local central bank mandates each impose specific technical controls that your stack must satisfy by design, not by workaround. Cross-border complexity adds another layer: multi-currency, multi-jurisdiction systems require FX handling, audit trails, and time-zone-aware scheduling built into the architecture from day one, not retrofitted under deadline pressure.

AI integration readiness is now a first-class requirement. Agentic workflows – fraud detection, automated lending decisions, portfolio rebalancing – need stacks with robust async patterns and observable state machines that support autonomous execution without sacrificing auditability. The user surface area matters equally: the performance demands of a retail consumer using a digital wallet and an institutional broker running desktop tooling differ enough that they can point toward entirely different stack choices.

Existing infrastructure gravity is the most underestimated factor. Greenfield teams can choose freely. For institutions carrying legacy systems, the true migration cost must be factored into any modernization roadmap before a single line of new code is written. The best stack on paper is rarely the right stack if it requires dismantling systems that the business cannot afford to pause.

Top 6 Finance Tech Stacks for Fintech App Development in 2026

1. Golang

The failure of high-frequency transaction systems is typically caused by their concurrency model, not hardware limitations.

When ledger updates, settlement events and fraud signals are arriving simultaneously at scale, thread-based architectures hit ceilings that no amount of additional compute can resolve. The demand for sub-second payment processing across multiple markets has made this a critical engineering problem, not a theoretical one.

By 2026, Golang has become the dominant language in fintech for building secure, high-throughput microservices and cloud-native backend systems. Its Goroutines – multiplexed over a small pool of OS threads by Go’s own runtime scheduler – enable tens of thousands of concurrent execution contexts with minimal memory overhead, making it the gold standard for services handling 100k+ TPS.

Profile-Guided Optimization (PGO) has become a serious cost lever for fintech teams running Go at scale. By feeding real production runtime profiles back into the compiler, the binary is optimized for actual workload patterns rather than theoretical ones – translating directly into measurable reductions in cloud compute costs across multi-region deployments, without a single line of application code changed.

In fintech, Go’s primary applications are real-time payment gateways, AI-based fraud detection pipelines, high-performance settlement infrastructure, and event-driven microservices where latency predictability under spike conditions is non-negotiable.

Sun* engineers rebuilt the core payment system for a $183M-funded MAS-licensed Embedded Finance platform from PHP to Golang while live. In this core banking modernization, operating across four Southeast Asian markets with no sandbox or documentation, our engineer team reverse-engineered the legacy logic to build the new Golang architecture in parallel.

2. .Net+Azure

Five Nines availability – 99.999% uptime – sounds like an infrastructure problem. In regulated financial environments, it’s equally a compliance problem: every unplanned outage is a potential regulatory reporting obligation, not just a business inconvenience.

As financial institutions face intensifying scrutiny across PCI-DSS, PSD2 and local central bank frameworks, the ability to demonstrate security controls under audit has become as important as the controls themselves.

.NET combined with Azure has established itself as the most defensible architecture for core banking and regulated financial workloads in 2026.

.NET 10’s performance improvements bring it within striking distance of Go for many backend workloads, while Azure Confidential Computing ensures data remains encrypted even while being processed in memory – a critical capability for handling customer PII and transaction data in shared cloud environments.

Azure Managed Identities eliminate long-lived credentials entirely and Azure Key Vault centralizes cryptographic key management with full audit logging, satisfying evidentiary requirements without bespoke engineering. Together, they enable zero-trust architectures that regulators can inspect, not just trust.

In fintech, .NET + Azure’s primary applications are core banking modernization, regulatory reporting systems, identity and access management, enterprise payment platforms, and any workload where compliance auditability is a first-class engineering requirement alongside performance.

Read our case study: Smarter Architecture Can Halve Bounce Rate | A Legacy System Modernization Case Study

3. React Native

The “feature gap” problem in digital wallets is more damaging than it appears on paper. When a biometric payment feature ships six weeks later on one platform, users don’t blame the platform – they lose confidence in the product. Maintaining separate iOS and Android codebases compounds the problem: longer release cycles, fragmented QA processes, and a development cost structure that consumes engineering capacity that should be directed at product differentiation.

React Native in 2026 – bolstered by its New Architecture featuring the Fabric rendering system and JavaScript Interface (JSI) – has become the leading cross-platform framework for fintech consumer applications.

Fabric introduces a synchronous rendering pipeline and enables concurrent execution of JavaScript and native code, closing the performance gap that previously made complex financial animations and authentication flows feel sluggish compared to fully native counterparts.

The React ecosystem’s depth in financial visualization tooling like charting libraries, real-time ticker components, portfolio heat maps means teams are composing from battle-tested components already running in production at major financial applications, rather than building bespoke data visualization infrastructure from scratch.

React Native’s primary applications are digital wallets, consumer banking apps, investment portfolio interfaces, payment confirmation flows, and any mobile product where feature parity across iOS and Android is a hard business requirement.

4. Flutter

Dated legacy insurance and investment apps look untrustworthy to younger, digitally-native users who expect the seamlessness of consumer apps. The core issue is structural: maintaining separate mobile, web, and desktop versions for the same product leads to an unsustainable maintenance burden and an inconsistent experience that damages brand trust.

Flutter has become the leading framework for fintech products that demand pixel-perfect UI consistency across mobile, web, and desktop from a single codebase.

The Impeller rendering engine – which compiles shaders at build time rather than runtime – eliminates the rendering jank that previously undermined trust in complex financial UIs, enabling consistent 120Hz smooth scrolling across dense investment portfolio views, real-time data grids, and interactive insurance dashboards.

Flutter’s “Write Once, Run Everywhere” maturity now genuinely extends to web and desktop, which matters specifically for insurance broker tooling where the same application logic must serve mobile-first retail policyholders and desktop-first broker workflows simultaneously.

In fintech, Flutter’s primary applications are insurance policyholder apps, investment portfolio platforms, wealth management dashboards, and any financial product where UI consistency across multiple platforms is a brand and trust requirement rather than just a technical convenience.

5. Java

The class of problems that breaks financial systems isn’t always speed – it’s correctness under pressure.

Complex state machines spanning multi-step loan origination flows, long-running settlement processes, and data integrity requirements that must survive hardware faults, network partitions, and partial writes demand a runtime where behavior is deeply predictable and failure modes are well-documented.

Many modern stacks optimized for throughput sacrifice the tooling maturity and type safety that these workloads require.

Java has reasserted its relevance for high-throughput financial backends through Project Loom’s Virtual Threads. By decoupling concurrency from OS threads, Virtual Threads allow Java applications to handle millions of concurrent I/O-bound operations – querying transaction histories, running credit risk models, generating regulatory reports without the thread pool complexity that previously pushed teams toward reactive frameworks and their associated cognitive overhead.

Spring Boot’s security modules remain the most extensively audited security framework in the financial software industry: when a regulator asks for documented evidence of authentication, authorization, and session management controls, Spring Security provides a clear, well-understood answer that bespoke implementations cannot match.

In fintech, Java’s primary applications are core banking backends, regulatory reporting engines, credit decisioning systems, complex transaction state machines, and any workload where long-term maintainability, type safety, and compliance auditability carry as much weight as raw performance.

6. Node.js

The user expectation in digital banking has fundamentally shifted. Push notifications for spending events, fraud alerts within 200ms of a suspicious transaction, live currency tickers that update without page refreshes.

Polling-based architectures cannot meet this expectation at scale without generating infrastructure costs that quickly become untenable, and traditional request-response patterns create latency profiles that users now experience as product failure.

Node.js has established itself as the preferred runtime for two distinct fintech use cases: real-time event orchestration and Agentic AI integration layers. Its single-threaded event loop and non-blocking I/O model are architecturally optimized for maintaining thousands of persistent WebSocket connections with minimal per-connection overhead – the exact workload pattern of a real-time financial notification service. On the AI front, the JavaScript ecosystem’s deep integration with LLM orchestration frameworks, combined with Node’s native handling of streaming token output via Server-Sent Events, makes it the most natural environment for building AI-powered financial assistants, automated alert systems, and conversational interfaces that interact with underlying fintech APIs.

Where Go wins on CPU-bound transaction processing, Node.js wins on I/O-bound connection management and AI orchestration at the application layer.

In fintech, Node.js’s primary applications are real-time notification services, WebSocket-based trading interfaces, Agentic AI wrapper layers, backend-for-frontend (BFF) orchestration, and live fraud alert systems where sub-200ms delivery is a product requirement.

Fintech Development Stack Comparison

A practitioner-level summary of how each stack performs across the dimensions that matter most in production fintech environments:

Tech Trends Shaping the Next 5 Years

The stacks discussed in this article will continue to evolve under pressure from shifts that are already visible in production systems today.

Agentic AI moves from experimental to infrastructure. Autonomous systems for financial transactions will be expected, not exceptional. Stacks that support observable, auditable AI execution pipelines will be crucial for satisfying both engineering requirements and regulatory scrutiny simultaneously.

ISO 20022 full adoption unlocks a compounding advantage. The global migration will unlock new capabilities. Systems using richer structured message data will enable advanced analytics and compliance automation superior to legacy MT-format integrations, significantly increasing the gap between early adopters and laggards.

Real-time expectations will spread beyond payments. Consumers now expect instant financial actions, including real-time balance updates, fraud decisions, and near-instant settlement. This real-time standard, prevalent in payments, is expanding into lending, insurance, and wealth management, leading to the obsolescence of batch processing for consumer-facing services.

Embedded finance rewards composability. The rise of financial services embedded into non-financial platforms will increase demand for lightweight, SDK-friendly stacks that integrate without requiring clients to adopt a full financial engineering toolchain. Institutions that architect for composability today will be the ones powering the next generation of embedded financial products.

Sun* possesses hands-on engineering expertise across all the tech stacks discussed in this article. We have a track record of delivering production fintech systems globally, spanning key areas like payments, digital banking, insurance, and investment management.

Our experience is valuable whether you are building a new architecture from the ground up or modernizing an existing core system.

Talk to our Fintech team.