React Native 0.76 marks a significant shift for mobile engineering teams. With the New Architecture now enabled by default, fintech companies are moving beyond a routine framework upgrade and into a broader infrastructure transition that impacts performance, security, compliance, and long-term platform stability.

For fintech applications, the migration carries additional complexity. Payment flows, biometric authentication, cryptographic operations, and PCI DSS-scoped systems all rely on predictable communication between JavaScript and native layers.

Changes introduced through Fabric, JSI, TurboModules, and bridgeless mode can influence not only user experience, but also SDK compatibility, security validation, and compliance readiness.

At Sun*, we work with fintech organizations navigating these architecture-level transitions in regulated environments.

This article explores what actually changed in React Native 0.76+ New Architecture, why the migration path differs for fintech products, and how engineering teams can approach performance optimization, security re-validation, and staged rollout planning with lower operational risk.

Key Takeaways

- React Native 0.76+ introduces major architectural changes through Fabric, JSI, TurboModules, and bridgeless mode, requiring fintech teams to rethink migration strategy beyond a standard framework upgrade.

- For fintech apps, migration impacts payment reliability, biometric authentication, RASP tooling, PCI DSS compliance, and third-party SDK compatibility – making security and validation critical.

- Successful migrations depend on phased rollout planning, dependency audits, TurboModule validation, and performance testing before exposing production payment flows to the New Architecture.

Why React Native 0.76+ Upgrade is different for fintech ?

Most React Native upgrade guides treat the New Architecture as a performance story. Install a flag, re-run your pods, enjoy smoother animations. For consumer apps, that framing is mostly accurate.

Fintech teams operate in a different environment, and that environment changes the risk calculus on every major platform change.

Regulatory overhead is real. PCI DSS v4.0, GDPR, and local financial authority requirements mean that a significant change to your mobile platform isn’t just a technical event , it’s potentially a compliance event. Changing the rendering engine and native module communication layer of your payment application may require documentation, testing evidence, and in some cases a conversation with your Qualified Security Assessor before the change goes to production.

Visual correctness is legally material. On a payment confirmation screen, a rendering glitch isn’t just a UX annoyance, it can create ambiguity about whether a transaction was completed. Under several financial regulations, unclear transaction feedback is a compliance issue. This means fintech teams need a higher bar for rendering correctness testing than a typical product team would apply.

Biometric authentication flows are deeply bridge-coupled. Face ID, fingerprint unlock, and step-up authentication during high-value transfers all depend on native modules that communicate with platform-level security APIs. The New Architecture fundamentally changes how JavaScript communicates with those modules and the threading model changes too. Flows that worked correctly under the old bridge need explicit re-validation under the new one.

App Store review cycles compress your testing window. For financial apps, Apple’s review process commonly runs five to ten business days. Google Play can be faster, but Play Protect policies add scrutiny to apps touching payment flows. The practical implication: if you find a regression after submission, your rollback options are limited and your fix cycle is measured in weeks, not hours.

None of this means you should delay the migration indefinitely. Legacy bridge support has a sunset trajectory, and the performance and security improvements in the New Architecture are real. But fintech teams need to approach this with a risk-aware process that goes beyond what a standard React Native migration guide recommends.

What Actually Changed in React Native 0.76+ New Architecture

To understand the fintech-specific implications of the New Architecture, you need a working mental model of what actually changed. The short version: three core systems were rebuilt from scratch and in React Native 0.76 they’re all enabled by default.

The old bridge and why it was a fintech bottleneck

The legacy React Native bridge worked by serializing all communication between the JavaScript thread and the native thread as JSON, passing messages across an asynchronous queue.

Every time your payment screen needed to read a value from a native module like checking biometric availability, querying the secure enclave, updating a balance tile that request had to be serialized, queued, delivered, deserialized, executed natively, re-serialized, queued again and delivered back to JavaScript.

For most UI operations, this was tolerable. For fintech-specific patterns, it created specific failure modes:

- Non-deterministic latency on animated balance tiles. The bridge queue has no priority system – a routine layout update and a critical transaction confirmation response compete equally for throughput. Under load, this produces visible jank that users associate with instability.

- Memory pressure from biometric data. Passing biometric image data from a native camera module through the bridge required full serialization – an expensive copy operation that put pressure on memory at the exact moment the UI should be most responsive.

- Callback chains on security operations. Every cryptographic operation – HMAC signing of API requests, token generation, secure enclave access – required an asynchronous callback chain. This made error handling complex and created timing windows that security-conscious teams had to reason carefully about.

The React Native 0.76+ New Architecture trio

React Native 0.76’s New Architecture is built on 03 components that work together to eliminate the bridge entirely.

JSI (JavaScript Interface) replaces the bridge with direct C++ host objects that are accessible from the JavaScript runtime without serialization. Your JavaScript code gets a reference to a native object and can call methods on it directly – the same way you’d call a method on any JavaScript object but the execution happens natively. No serialization, no queue, no round-trip.

Fabric is the new concurrent renderer. Built on top of React 18’s concurrent rendering primitives, Fabric moves shadow tree calculation (the layout computation step) to a background thread, then commits layout changes to the native view layer synchronously. This eliminates the race conditions that caused the “flash of unstyled content” and the jank visible on balance updates and modal transitions.

TurboModules replace the old NativeModules system. Where NativeModules were eagerly initialized at startup (contributing to slow cold starts), TurboModules are lazy, they initialize the first time they’re called. They also support synchronous initialization and synchronous return values via JSI, which is directly relevant to biometric auth flows and cryptographic operations.

Bridgeless mode – the default in 0.76 – removes the legacy bridge entirely. There is no fallback channel. When bridgeless mode is active, any native module that hasn’t been migrated to TurboModules simply doesn’t work. This is the source of most migration failures for teams that haven’t done a thorough dependency audit.

JSI in fintech: the synchronous access story

The most practically significant change for fintech applications is JSI’s synchronous access model. Under the old bridge, there was no way to get a synchronous return value from a native operation, everything was callbacks or promises. JSI changes this.

A biometric authentication check that previously required an async callback chain can now be implemented as a synchronous call that resolves within a single event loop tick. An HMAC signing operation that had to be wrapped in a Promise chain for timing reasons can now return its result synchronously to the calling code.

This matters for payment flows specifically because authentication and cryptographic operations appear at critical junctures – right before a transaction is submitted, right before a high-value transfer is confirmed. Asynchronous chains at those junctures create complexity that has historically been a source of bugs, race conditions, and in some cases security issues.

One important caveat: synchronous JSI calls block the JavaScript thread. Any TurboModule that takes more than roughly five milliseconds to return will cause dropped frames.

Before exposing any native crypto operation synchronously, profile it with Android Systrace or iOS Instruments. Operations that run longer – full certificate chain validation, large-payload HMAC computation should still be dispatched to a native background thread and return their results asynchronously, even under the new model.

Third-party SDK compatibility at the time of React Native 0.76+ New Architecture varies. The Stripe React Native SDK publishes explicit New Architecture support. Plaid Link and several KYC/AML providers have been slower to update their native wrappers – verify the current status of every SDK in your dependency tree before committing to a migration timeline.

Performance Gains and Security Tradeoffs on Payment Screens

Concrete performance wins for payment UX

Synchronous layout commits on confirmation screens. Fabric commits all payment confirmation state changes to the native view layer atomically. Under the old Paper renderer, those updates arrived across multiple async frames, producing a flicker that some users interpreted as the transaction failing.

React 18 Transitions for real-time data. Transition lets you mark forex rate updates and transaction feed refreshes as deferrable, so they never interrupt a tap on a “Buy” button or a biometric prompt. The UI prioritizes what the user is actively touching.

P99 frame consistency over average FPS. One dropped frame at the moment a user taps “Confirm Payment” is perceptible and erodes trust. Fabric’s deterministic commit model significantly improves P99 consistency, especially on mid-range Android devices common in emerging market fintech user bases.

Where Fabric does not help

Network-bound latency is unchanged – Fabric is a rendering optimization only. Cold start, dominated by JS bundle parse time, also isn’t materially improved; address that separately with Hermes bytecode precompilation.

And concurrent features require disciplined component architecture to realize their benefit – a poorly structured payment form won’t suddenly perform well under Fabric.

The security surface area shift with bridgeless mode

The old bridge’s serialized message queue was observable on rooted or jailbroken devices – a known attack vector for intercepting session tokens and payment credentials. Bridgeless mode eliminates that queue entirely.

The tradeoff: any JavaScript executing in your app can now synchronously call any registered JSI host object. A compromised npm package has a direct, synchronous path to your secure enclave module, biometric auth module, and certificate store. Apply least-privilege principles to your TurboModule registry – don’t register native capabilities that the JS layer doesn’t strictly need.

RASP tools are the most urgent concern. Products like Appdome and Guardsquare instrument the bridge for tamper and root detection. Those hooks stop working in bridgeless mode. Get written confirmation from your vendor before migrating any production build that relies on RASP for compliance – this is a program blocker, not a nice-to-have.

For TurboModules wrapping Secure Enclave or Android Keystore: return operation results only – never key handles or key material. The JS layer should never be able to extract a secret through a TurboModule call.

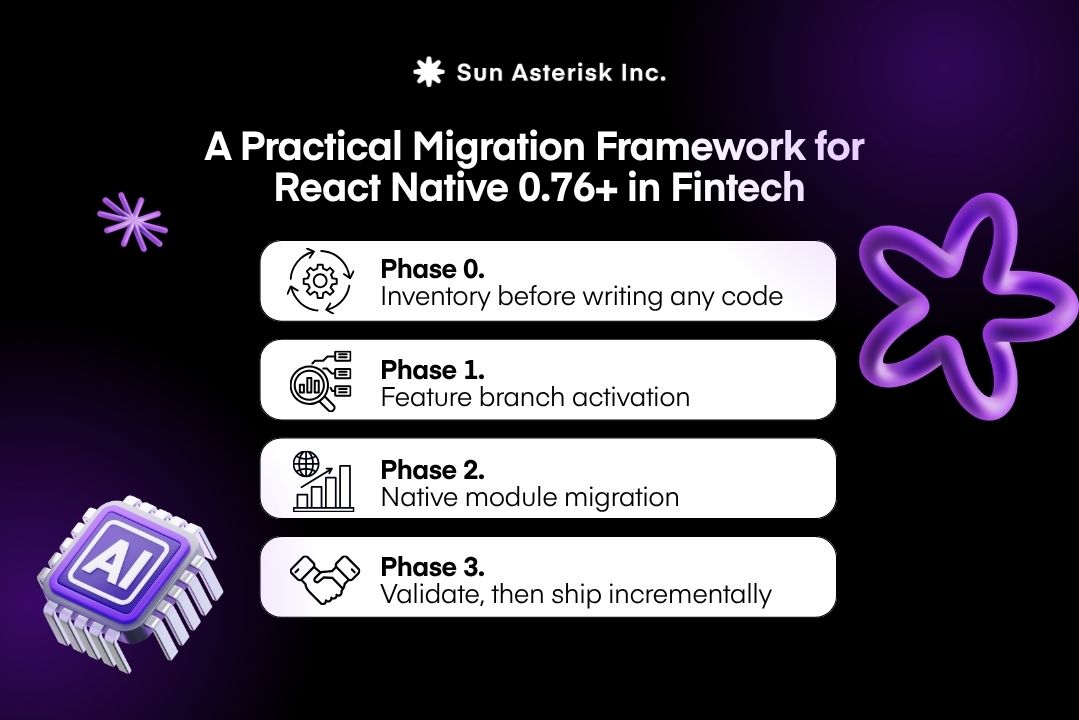

A Practical Migration Framework for React Native 0.76+ New Architecture in Fintech

A fintech New Architecture migration is a program, not a sprint. The teams that get into trouble treat it like a library upgrade. The teams that succeed treat it like an infrastructure change – phased, gated, and validated before production traffic sees a single line of new code.

Phase 0. Inventory before writing any code

The output of this phase is a go/no-go decision and a complete dependency map.

Grep your codebase for every NativeModules.X call – these are all legacy bridge calls that need migration or wrapping. For every third-party native SDK in package.json, check GitHub release notes for explicit New Architecture support language. “Supports React Native 0.70+ New Architecture” is not the same as “supports TurboModules” – check the actual releases, not the top-level README.

Build a compatibility spreadsheet: SDK name, NA support status, internal owner, remediation estimate, and blocking/non-blocking classification. A payment gateway SDK not compatible is a hard blocker. An analytics SDK is not – use a shim and migrate it later.

Contact your RASP vendor in writing. Get explicit confirmation of bridgeless support and the minimum RN version validated. If they can’t confirm, treat this as a program blocker before moving to Phase 1.

Phase 1. Feature branch activation

Enable New Architecture on a dedicated branch – never on main until migration is complete and validated.

Run your full automated test suite immediately. Categorize every failure – New Architecture regression vs. pre-existing issue. This baseline is essential: you need to know exactly what the flag broke versus what was already broken.

Use React Native DevTools (0.76+) to watch TurboModule initialization and Fabric layout events. Any module that silently fails to initialize here will silently fail in production later.

Phase 2. Native module migration

Migrate custom native modules to TurboModules in fintech priority order: biometric auth first (on the critical path for every transaction), then certificate pinning, then cryptographic helpers (HMAC signing, secure enclave access), then analytics and logging last – these can run on a compatibility shim while higher-priority modules are completed.

Use react-native-codegen to generate TypeScript specs and native stubs. Codegen enforces type safety at the interface boundary, which matters for security-sensitive modules where argument type confusion has been a real vulnerability class.

Test each TurboModule in isolation before plugging it back into payment flows. Write unit tests covering the interface contract, not just the happy path — for crypto modules, include edge cases: empty input, oversized payloads, malformed keys.

Phase 3. Validate, then ship incrementally

Before any production rollout, run three validation passes.

Performance: Profile the full checkout flow on your P50 device – not your development machine. Measure P50, P95, and P99 frame times for the payment form, biometric prompt, and confirmation screen against your pre-migration baseline. A P99 regression on the confirmation tap is a ship-stopper.

Security: Re-run your RASP validation suite. Confirm root detection, jailbreak detection, and tamper detection all produce correct results in bridgeless mode. Then run a focused pen test: can a compromised JS dependency reach sensitive TurboModules synchronously? Verify the answer is no before shipping.

Rollout: 10% traffic → 72 hours monitoring → 50% → 48 hours → 100%. Retain legacy build artifacts for one full release cycle as a rollback option. Document the migration as a significant change – what changed, what was tested, who approved – for PCI DSS evidence if your QSA asks.

Should we upgrade React Native 0.76+ New Architecture now?

RN 0.76 supports interoperability layers that let legacy bridge modules keep functioning while the rest of the app runs on New Architecture. This is a valid incremental strategy – ship Fabric and JSI benefits to your main UI flows while one or two lagging SDKs catch up.

One caveat: bridge-layer RASP hooks may fail in unpredictable ways in hybrid mode, which is harder to diagnose than a clean break. Resolve RASP compatibility before relying on the hybrid path in production.

| Signal | Upgrade now | Phase it in | Wait |

|---|---|---|---|

| RN version | 0.73+ with New Arch opt-in already tested | 0.71-0.72 | Below 0.71 |

| SDK compatibility | >80% compatible, no payment-critical gaps | 1-2 non-critical SDKs lagging | A payment gateway or KYC SDK has no NA support or timeline |

| RASP tooling | Vendor confirmed bridgeless support in writing | Vendor in active validation | Vendor cannot confirm – bridge hooks will break |

| PCI DSS status | No active assessment, or QSA has reviewed the change | Assessment ending in >60 days | Mid-cycle assessment, QSA not yet engaged |

| Team capacity | 6-8 weeks with dedicated QA + security review | Can run incrementally over a quarter | No migration bandwidth in current roadmap |

| Performance pressure | Active jank complaints on payment screens | Moderate – worth fixing this cycle | None – stable, no user-facing urgency |

React Native 0.76+ New Architecture is a genuine step forward for fintech – better payment screen reliability, simpler security-critical module design, and a smaller bridge-interception attack surface but it’s a program, not a flag flip.

The teams that come out ahead are the ones who start the dependency audit before they’re under pressure, confirm RASP compatibility in writing, and treat staged rollout as non-negotiable. The architecture is ready; the question is whether your team and your SDK stack are.

Our experience at Sun* involves assisting fintech organizations with intricate React Native 0.76+ New Architecture migrations. We provide comprehensive support throughout the process, including conducting thorough dependency audits, performing TurboModule rewrites, and managing essential security re-validation alongside detailed compliance documentation.

Get in touch with our team.