Most enterprise security teams aren’t negligent. They’re skilled, thorough, and operating in the wrong threat model.

The table stakes are covered — SSL/TLS enforced, authentication flows rigorously implemented, sensitive data encrypted at rest. For a web application, that’s a defensible posture. For a fintech mobile app, it’s where the real work begins.

At Sun*, during the process of working with clients’ fintech mobile apps, we found the hard truth that mobile is not a constrained browser. It’s a compiled binary running on hardware you don’t control, inside a runtime environment that a motivated attacker can instrument and manipulate at a depth no web session ever exposed. That distinction matters more than most security architectures currently reflect.

Meeting the real fintech app security requirements means recognizing that breaches don’t arise from simple errors like missing HTTPS — they arise from dangerously applying web-centric security assumptions to a platform with fundamentally different trust conditions. Binary exposure, hostile runtimes, UI-layer deception, compromised third-party SDKs: none of these fit neatly into a web-era threat model, which is precisely why they keep slipping through.

Your security model may be comprehensive. The harder question is whether it was built for the platform you’re actually defending.

Key takeaways

- Mobile apps have a unique, more vulnerable attack surface than web apps. Standard web-era defenses (SSL, encryption, auth) are inadequate.

- Your compiled mobile binary is easily decompiled, exposing hardcoded secrets, API keys, and business logic, despite language safety (Kotlin, Swift).

- The client device is untrusted; runtime tools like Frida can bypass defenses and extract keys from memory, making client-side protection unreliable.

- Third-party SDKs, often overlooked, pose a significant blind spot due to deep permissions and minimal oversight.

Why Fintech App Security Requirements Go Further Than Other Apps?

Fintech mobile apps carry sensitive data and financial consequences. A single exploited vulnerability isn’t a support ticket; it’s a regulatory investigation, a breach disclosure, and a customer trust problem that compounds long after the technical fix is deployed.

The stakes are categorically different from other consumer apps, and the security bar has to reflect that.

The attack surface alone demands a different posture. Unlike a web application where the perimeter is relatively contained, mobile introduces threat vectors at every layer – the OS, the hardware, the network, and the application itself.

Attackers don’t need to find one way in, they have four. And the numbers reflect that reality: a 2025 industry report found that 87.5% of financial services apps experienced an attack within a single month.

Then there’s the regulatory dimension, which doesn’t forgive gaps that the market might have tolerated. PCI-DSS governs how payment data moves and rests. GDPR dictates how personal data is handled and disclosed.

Regional frameworks like the EU’s DORA and local banking regulations add jurisdictional layers that vary by market. Non-compliance isn’t a technical debt item, it’s a financial liability with a fixed penalty structure and no grace period.

Most teams understand the stakes. Where they fall short is execution, specifically, 05 security requirements that consistently get deprioritized, misunderstood, or missed entirely.

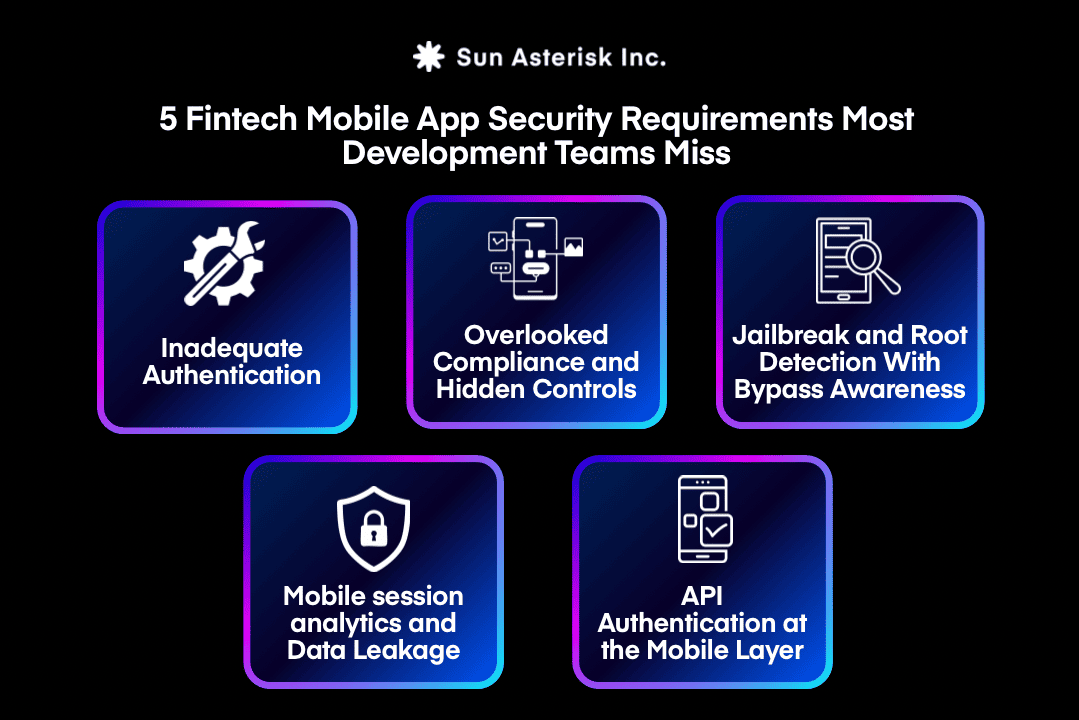

5 Fintech Mobile App Security Requirements Most Development Teams Miss

Requirement 1. Inadequate Authentication

Inadequate authentication covers two failure modes that are almost always treated separately — but in practice, they reinforce each other’s weaknesses. Weak authentication gives attackers a way in. The absence of runtime protection means they can stay in, undetected, doing damage your server-side controls will never see.

Most fintech teams implement what they were already using: passwords plus SMS-based two-factor authentication. It’s familiar, it ships fast, and it feels secure. The problem is the industry has largely moved on from both. Passwords are routinely compromised through credential stuffing and phishing.

SMS 2FA is vulnerable to SIM-swapping — a technique requiring no technical sophistication, only a social engineering call to a mobile carrier. If your authentication security depends on the integrity of a carrier’s customer support process, how confident are you in that foundation?

What teams miss is the shift toward authentication models that bind identity to the device itself. Passkeys — the FIDO2/WebAuthn standard — eliminate the shared secret entirely. Authentication is performed through a cryptographic key pair where the private key never leaves the user’s device, biometric verification unlocks it locally, and nothing sensitive is transmitted. This isn’t a future-state aspiration — it’s a production-ready standard on both iOS and Android that eliminates entire categories of credential-based attacks at the architecture level.

The second failure mode runs deeper. Even with strong authentication at the door, most security architectures are built around the perimeter — and that is precisely what sophisticated attackers have learned to avoid. Runtime Application Self-Protection addresses this gap directly.

Rather than a wall around your application, RASP functions as an immune system within it, detecting and responding to threats at execution time. Without it, your app is exposed to method hooking, dynamic instrumentation via tools like Frida, and memory tampering that bypasses in-code validation entirely.

Web-centric AppSec tools and source code scanners never see the compiled artifact your users actually run — hardcoded secrets and cryptographic misconfigurations only become visible at the binary layer. At minimum, your RASP implementation should detect debugger attachment, validate code checksums, and flag dynamic library injection. Together, strong authentication and runtime protection close a loop that neither can close alone — making your app a far less attractive target.

Requirement 2. Overlooked Compliance and “Hidden” Controls

Most fintech teams treat compliance as a backend concern — something infrastructure owns, with the mobile app as a downstream consumer of whatever security guarantees the server provides. This framing is costly. PCI DSS and GDPR don’t stop at the API boundary. They extend into the app’s architecture: how cardholder data is handled in memory, how user consent is captured locally, how sensitive fields are rendered on-screen. Ignoring the mobile layer’s compliance surface doesn’t make those requirements disappear — it just means they surface during an audit instead of a design review.

The second gap is structural. Most teams rely on manual, periodic security audits — which measure a point in time, not a continuous state. Code ships between audits. Dependencies update. Configuration drifts. Understanding the full scope of fintech app security requirements means recognizing that compliance isn’t a milestone you reach — it’s a state you maintain. The fix is to move security testing into the CI/CD pipeline itself, running automated checks on every build so compliance regressions are caught at the commit level, not the quarterly review.

Certificate pinning illustrates both problems perfectly. The distance between “we have pinning” and “our pinning actually works” is vast, and audits regularly expose that gap. The most common failure isn’t skipping pinning entirely — it’s pinning only the leaf certificate, then quietly removing the pin during an emergency hotfix when the cert rotates and the app breaks. What remains is the appearance of a control without the substance of one. Effective pinning anchors to both the leaf and at least one intermediate CA, includes automated expiry alerts in your DevOps pipeline — 60 days minimum — and is regularly verified against proxy bypass tools on compromised devices. That last step is where pipeline automation earns its place: a pinning validation test on every release build makes regression impossible to miss.

Requirement 3. Jailbreak and Root Detection With Bypass Awareness

Almost every fintech app implements jailbreak and root detection. Almost none implement it in a way that holds against a motivated attacker — and the gap between those two statements is where breaches happen.

Checking for Cydia, /etc/apt, or su binaries was a reasonable approach in 2015. Today, tools like Magisk on Android and Liberty Lite on iOS exist specifically to defeat these checks — hiding modification artifacts, spoofing filesystem responses, and in some cases patching detection logic in memory before it executes. Static artifact checks will catch unsophisticated attempts. They will not catch someone who is specifically targeting your application.

This is one of the fintech app security requirements that exposes a deeper architectural misunderstanding: client-side detection should never function as a trust boundary. Root and jailbreak checks add friction — valuable friction — but critical authorization and validation must live server-side, because a motivated attacker controls the client’s runtime environment entirely. Treating client-side signals as authoritative is the mistake.

The effective approach layers behavioral signals — anomalous process spawning, timing discrepancies, unexpected memory permissions — with native-layer checks that are significantly harder to bypass than Java or Swift-layer equivalents. And every evasion attempt, successful or not, should be logged server-side. The attackers who almost bypassed your detection tell you more about your actual exposure than the ones you blocked cleanly.

Requirement 4. Mobile Session Analytics and Data Leakage

Teams encrypt sensitive data at rest and consider the requirement satisfied. The problem is that encryption is only as strong as the security of its key — and the key is usually the part that isn’t handled well. AES-256 means very little if the key lives in SharedPreferences or UserDefaults in plaintext, adjacent to the data it’s supposed to protect.

The fix is non-negotiable: generate and store keys inside the Android Keystore or iOS Secure Enclave, where they cannot be extracted even on a compromised device. Sensitive data that doesn’t need to persist locally shouldn’t be cached at all — avoiding these gaps is one of the most overlooked fintech app security requirements in mobile development today. Avoid storing PII, session tokens, or financial identifiers in local storage without an explicit, justified reason.

The leakage vector most teams don’t model is their own analytics tooling. Session replay and screen recording SDKs capture everything rendered on screen unless explicitly configured otherwise — in a fintech app, that includes banking IDs, account numbers, and KYC screens. The typical approach is privacy-by-exception: mask the fields someone remembers to flag. The correct approach is privacy-by-default: all data masked unless intentionally allowed. The distinction sounds minor. In practice it’s the difference between a compliant implementation and one quietly exfiltrating customer financial data to a third-party platform.

Beyond key management, the remaining leakage vectors are unglamorous but routinely exploited: clipboard persistence across apps, debug logs containing tokens that should be failing CI pipelines instead of appearing in incident reviews, missing screenshot protection on sensitive screens, and unsanitized UI state exposed through the app switcher on backgrounding. None of these are exotic — they’re the details that separate a security-conscious implementation from one that checked the encryption box and moved on.

Requirement 5. API Authentication at the Mobile Layer

JWT-based authentication is the industry default and it works — until someone steals the token. In the mobile context, token theft doesn’t require a server breach.

Memory scraping, log exposure, and insecure local storage all create viable extraction paths. Once an attacker holds a valid JWT, your backend has no mechanism to distinguish their requests from your user’s.

This is the architectural blind spot most fintech teams carry into production: treating the token as the identity. The more precise question isn’t whether a token is valid, it’s whether a valid token is being presented by the legitimate device and user it was issued to. Those are different questions with fundamentally different security outcomes.

Mutual TLS addresses the device authenticity problem at the handshake layer, requiring the client to present a certificate rather than just the server. Your backend can then cryptographically verify that requests originate from a genuine installation of your app, not just from someone in possession of extracted credentials.

Token binding to device fingerprint adds a second layer: tokens become non-transferable between devices, eliminating the replay attack vector even if extraction occurs.

For internal microservices traffic, mTLS should be non-negotiable. The internal network is not a trust boundary, and treating it as one is how lateral movement after an initial compromise reaches your most sensitive data.

Security at the mobile layer doesn’t end at the app, it has to extend through every hop in the chain.

Prioritizing Fintech App Security Requirements for Your Team

Not every team has the bandwidth to implement all five requirements in the next sprint. A practical prioritization framework leverages both risk exposure and the cost of implementation — start with the controls that close the widest gaps at the lowest implementation cost, and build from there.

Solid SSL, encryption, and authentication aren’t enough. Fintech app security requirements extend well beyond what web-era controls were designed to cover — from decompilable binaries to runtime instrumentation to unsupervised third-party SDKs. The gaps are real, exploitable, and routinely missed by teams that are otherwise doing everything right. Securing mobile fintech means treating the client device as untrusted from the ground up, not as a trusted extension of a secure backend.