The financial industry has never been short of technology promises. But generative AI is proving to be something different – not a tool that merely automates what humans already do, but one that fundamentally changes what is possible at scale.

For fintech companies, the timing is significant. A sector built on data, trust, and operational precision now has access to AI systems that can read contracts, explain fraud patterns, generate compliant training datasets, and hold sophisticated financial conversations in any language without proportional increases in cost or headcount.

At Sun*, we’ve worked alongside fintech teams across Asia to design and build products at this intersection. What we’ve observed firsthand mirrors what the data confirms: the organizations generating real returns from generative AI aren’t the ones with the biggest budgets. They’re the ones with the clearest use cases, the strongest data foundations, and the discipline to scale what works.

In this article, we’ll break down where generative AI is delivering proven value in fintech today and how to build a path toward it.

- Generative AI is moving from experimentation to production across fintech, with clear ROI in support, compliance, and engineering.

- The biggest gains come from augmenting – not replacing – existing systems and teams.

- High-impact use cases cluster around document-heavy workflows, customer interaction, and developer productivity.

- Success depends less on the model itself and more on governance, data strategy, and integration into real operations.

What Generative AI actually means in Fintech?

Generative AI is not simply “smarter software.” It represents a fundamental shift in how machines process and produce information. Where traditional AI predicts and classifies – flagging a transaction as suspicious, scoring a credit application – generative AI reasons, creates, and explains.

| Capability | Traditional/Predictive AI | Generative AI |

| Core function | Classifies, predicts, scores | Creates, reasons, generates |

| Input | Structured data (numbers, labels) | Unstructured data (text, images, documents) |

| Output | A score, a label, a decision | Written content, code, synthetic data, dialogue |

| Example in fintech | Credit scoring model | AI that explains why a loan was declined – in plain language |

| Strength | High accuracy on well-defined tasks | Flexible reasoning across ambiguous, complex tasks |

In practical fintech terms, generative AI delivers four core capabilities that were simply not available at scale before:

- natural language generation (producing human-readable explanations, reports, and responses),

- code generation (accelerating engineering velocity),

- synthetic data creation (solving the training-data problem without violating privacy),

- and document understanding (reading, extracting, and acting on unstructured documents)

Why Fintech is a Prime Use Case

Fintech offers the ideal conditions for generative AI adoption. It combines large volumes of data, heavy regulatory demands, and constant pressure to improve customer experience – creating clear, high-value opportunities for automation and intelligent decision-making.

As a result, generative AI is not just experimental in fintech, it is rapidly becoming a core capability across operations, compliance, and customer engagement.

- Data-rich environment: Financial institutions generate vast volumes of both structured and unstructured data-ideal for training and deploying AI systems.

- High compliance and documentation burden: Processes like KYC, AML, and reporting are document-heavy and repetitive, making them prime candidates for automation.

- Customer experience pressure: Users expect real-time, personalized, and seamless financial services across channels.

- Constant demand for operational efficiency: Margins are under pressure, pushing firms to automate workflows without compromising compliance or accuracy.

Where Generative AI Is Already Working in Fintech

1. Automated customer support and conversational banking

Modern AI chatbots have moved far beyond scripted FAQ responses. Powered by LLMs, they can handle nuanced queries about account terms, dispute resolution workflows, and product eligibility in any language, at any hour.

More significantly, they can deliver proactive, personalized financial guidance based on a customer’s spending patterns and stated goals, a capability that was previously reserved for high-net-worth private banking clients.

Multilingual support at scale is a particular breakthrough for fintech companies operating across Southeast Asia, where language fragmentation has historically limited service quality. AI-driven interfaces reduce support ticket volumes and significantly improve customer satisfaction scores without proportional headcount growth.

2. Intelligent Document Processing & Compliance

KYC onboarding and AML document review remain among the most manual and error-prone workflows in financial services.

Generative AI fundamentally changes this by enabling systems to read, extract, cross-reference, and flag information across a wide range of documents: passports, utility bills, business registrations, and beneficial ownership declarations with a level of speed and consistency that manual review struggles to achieve.

Instead of relying on fragmented OCR and rule-based tools, generative models can understand context across documents, detect inconsistencies, and escalate risks in real time. This significantly reduces onboarding friction while strengthening compliance accuracy.

Beyond onboarding, document intelligence reshapes how compliance teams handle large volumes of complex information. Contracts, regulatory updates, and audit reports – traditionally time-intensive to review – can be processed and distilled into structured insights.

AI systems can highlight material clauses, identify anomalies, and generate concise summaries, effectively turning a 200-page bond indenture into an actionable brief within minutes.

The result is not just efficiency, but a shift in how compliance operates: from reactive document processing to proactive risk identification and decision support.

3. Fraud Detection & Risk Analysis

Generative AI does not replace existing fraud detection models, it strengthens them in ways that directly address long-standing gaps in risk and compliance.

First, it enhances explainability. Traditional ML models often operate as black boxes, making it difficult for analysts and regulators to understand why a transaction was flagged.

Generative AI can translate these outputs into clear, human-readable explanations, enabling faster decision-making and stronger auditability. This capability is becoming increasingly critical as regulatory frameworks, such as the EU AI Act, place greater emphasis on transparency in high-risk systems.

Second, and more strategically, generative AI enables adversarial training through synthetic data. It can simulate realistic fraud scenarios, new attack patterns, behavioral anomalies, and edge cases that do not yet exist in historical datasets.

By exposing detection models to these scenarios, institutions can proactively strengthen their defenses against emerging threats.

In practice, this approach has delivered measurable results. Some large-scale platforms have reported up to a 40% reduction in fraud losses by training models on synthetic edge cases that real-world data alone could not capture.

Read more: How Real-Time Fraud Detection and Prevention in Banking Industry Works via Millisecond ML Scoring

4. Personalized financial products and marketing

Dynamic product recommendation is one of the clearest ROI stories in fintech AI. Rather than relying on broad demographic segmentation, generative AI systems synthesize behavioral signals, transaction history, and life-stage indicators to match each user with the most relevant financial product at the moment it matters most.

This level of precision extends into marketing execution. AI-generated content – personalized emails, in-app messages, and push notifications – can be tailored at the individual level, far beyond what traditional campaign structures or human copywriting teams can scale. Messaging becomes contextual, timely, and aligned with real user intent rather than predefined segments.

At the same time, robo-advisory services powered by generative AI are gaining mainstream adoption, managing billions in assets globally. User trust is also shifting: a growing share of customers now report trusting algorithmic recommendations as much as or more than human advisors when the experience is transparent and consistent.

The outcome is straightforward: higher conversion rates, deeper engagement, and improved long-term retention – driven not by more outreach, but by more relevant interactions.

5. Developer productivity and fintech engineering

The impact of generative AI on software development velocity is one of the most underappreciated ROI drivers in enterprise technology.

For fintech engineering teams – tasked with building and maintaining payment integrations, API connectors, regulatory reporting pipelines, and real-time processing systems – code generation significantly compresses delivery timelines.

Generative AI can produce API scaffolding, integration logic, and even infrastructure templates, allowing engineers to focus on higher-value architecture and problem-solving.

Beyond code generation, capabilities such as automated documentation, intelligent code review, and AI-assisted debugging create compounding efficiency gains across the entire development lifecycle.

In practice, workflows that previously took weeks, such as shipping a new API integration, can now be completed in a fraction of the time. Automated test generation and compliance-focused code scaffolding further reduce the risk of human error, which is critical in high-stakes regulatory environments.

The competitive implication is clear: faster development cycles translate directly into shorter time-to-market, increased engineering throughput, and lower cost per feature without compromising system reliability or compliance.

6. Synthetic data for model training

Privacy regulations such as GDPR, PDPA and the growing patchwork of Southeast Asian data protection frameworks create a fundamental constraint for AI development in fintech: access to usable, compliant data. In many cases, real customer data cannot be freely used for training without introducing legal and ethical risk.

Synthetic data offers a practical path forward. These are artificially generated datasets that retain the statistical properties and patterns of real data without exposing any individual-level information. As a result, they enable model development while preserving privacy and regulatory compliance.

Generative AI significantly advances this capability. Modern models can produce highly realistic transaction histories, customer profiles, and financial scenarios, providing machine learning teams with the scale and diversity of data required to train robust systems. They can also simulate rare or extreme conditions- edge cases that are difficult to capture in real-world datasets but critical for model performance.

This approach addresses two of the most persistent barriers in financial services AI: regulatory constraints and data scarcity. By decoupling model training from sensitive data, synthetic data enables faster experimentation, safer collaboration, and more scalable AI adoption.

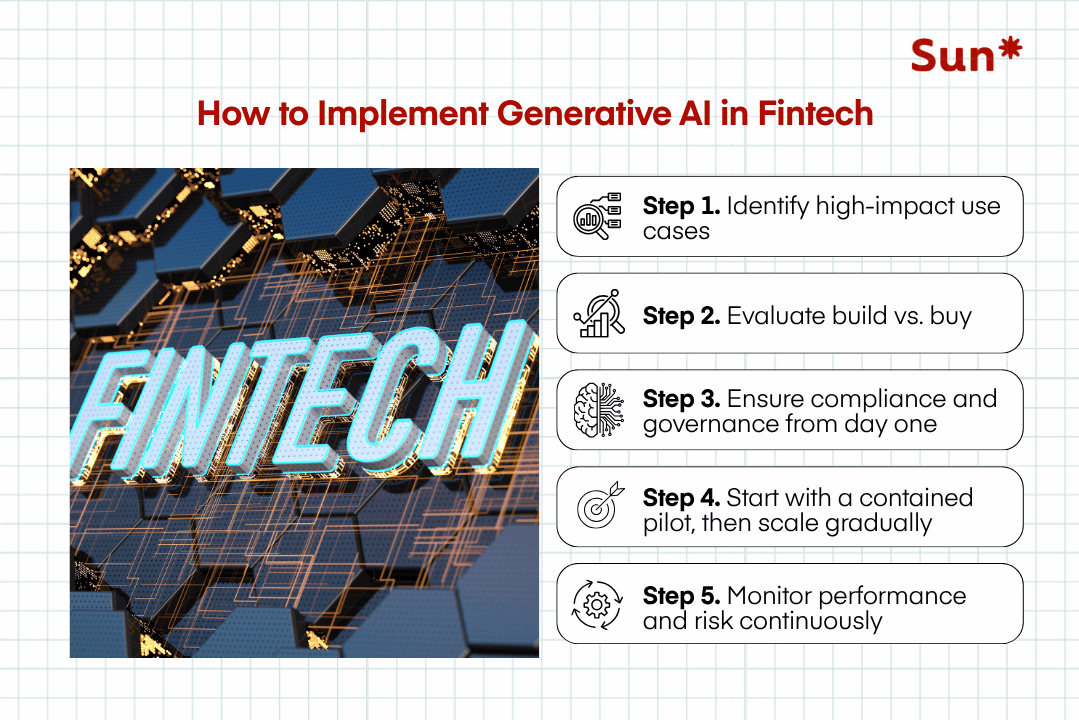

How to Implement Generative AI in Fintech

Step 1. Identify high-impact use cases

Map AI opportunities to specific operational pain points with quantifiable costs – not abstract aspirations. Where are humans doing repetitive, document-heavy, or time-sensitive work? That is your starting list. Prioritise by potential impact multiplied by implementation feasibility.

Step 2. Evaluate build vs. buy

For commodity capabilities (conversational AI, document extraction), buy or partner with best-in-class providers. Reserve engineering investment for use cases where proprietary data gives you a differentiated edge. Most fintech firms benefit from a hybrid approach: hosted LLMs fine-tuned on proprietary data via API.

Read more: Build vs. Buy Decision for Fintech: A 2026 framework

Step 3. Ensure compliance and governance from day one

Define your AI governance framework before writing a line of production code. This includes data residency policies, model documentation standards, bias testing protocols, and escalation pathways for edge cases. Build compliance in, not on.

Step 4. Start with a contained pilot, then scale gradually

The 2026 industry shift is from isolated AI experiments to enterprise-wide programmes. The fastest path there is not to launch everywhere at once – it is to run one rigorous pilot with defined success metrics, prove the model, then replicate. Successful firms adopt modular AI architectures that allow rapid iteration without systemic risk.

Step 5. Monitor performance and risk continuously

AI models degrade. Data distributions shift. Regulations change. Production AI in fintech requires ongoing monitoring of model accuracy, output quality, bias indicators, and compliance alignment – not just at launch, but permanently. Embed model audit tooling directly into ML pipelines to catch drift before regulators do.

What’s Next: 05 Trends Shaping Generative AI in Fintech

1. Agentic AI

The next frontier is not AI that responds to queries, it is AI that initiates actions. Agentic AI systems can autonomously execute multi-step workflows: reviewing a credit application, requesting additional documentation, running fraud checks, and routing for human approval, all without manual orchestration. The AI agent market is projected to reach $52 billion by 2030 at a 46% CAGR, and co-pilots are expected to be integrated into 80% of enterprise applications by 2026.

2. From Pilots to Enterprise-Wide AI Programmes

The defining shift of 2026 is the move from isolated AI experiments to modular, enterprise-scale deployment. Successful institutions are adopting unified AI platforms combining fraud analytics, customer support, and governance controls in a single control plane and measuring outcomes through live business metrics rather than lab benchmarks.

3. Regulation as architecture, not constraint

DORA, the EU AI Act, PSD3, and equivalent frameworks in Singapore and beyond are reshaping how AI systems are designed, not just deployed. Explainability, model transparency, and bias mitigation are becoming baseline requirements for high-risk financial AI applications.

The most sophisticated institutions are turning regulatory compliance into a design advantage – building auditable, trustworthy systems that competitors cannot easily replicate.

5. Synthetic data matures into infrastructure

Synthetic data is transitioning from a niche workaround to core AI infrastructure. As privacy regulations tighten and demand for model training data grows, the ability to generate high-fidelity synthetic financial datasets will become a standard capability in every serious AI team’s toolkit.

The market for synthetic data in financial services is growing alongside the broader AI infrastructure buildout, which attracted over $202 billion in venture funding in 2025 alone. Organizations that invest in synthetic data capabilities now will have a compounding advantage in model quality and regulatory compliance as the decade progresses.

Moving Generative AI from experimental phases to tangible business outcomes

Generative AI has transitioned from a fintech experiment to a core value driver across customer experience, risk management, and software engineering. Leadership in this era is no longer defined by the volume of pilots, but by the precision of execution – prioritizing high-impact use cases, rigid governance, and seamless, scalable integration.