Fintech and insurtech have moved past the 2022–2024 era of AI curiosity. By 2026, AI is the operational core of competitive financial institutions, making execution speed paramount.

Major carriers and Tier-1 banks are now demanding a shift from generative chat to agentic AI — systems that enable autonomous decisions, complex workflow management, and transaction execution without constant human intervention.

For financial institutions at this inflection point, the build vs. buy decision for fintech is now critical: a poor choice means lost technology and a lag behind agile competitors. Investment is shifting from “AI-enabled” pitches to companies demonstrating real-time AI impact on loss ratios or customer acquisition costs.

At Sun*, we work with financial institutions navigating exactly this inflection point. In this article, we break down the strategic framework for deciding which technology layers to own, which to buy, and what the stakes of getting it wrong look like in 2026.

Key takeaways

- The “Build vs. Buy” decision is now a three-way choice: Build, Buy, or Acquire, each with unique, irreversible consequences.

- A narrowed early-stage vendor pipeline makes the “just buy it” path significantly riskier.

- LLMs and the Model Context Protocol are redefining distribution; companies not AI-optimized risk losing customer segments.

Why 2026 Marks the Permanent Build vs. Buy Decision for Fintech

The traditional binary of “build vs. buy” has evolved into a multi-path framework – build, buy, acquire, or strategically partner and each path carries asymmetric risks that make the choice harder to reverse than ever before.

What to build?

Building in-house offers maximum control but demands maximum commitment. Annual investment for even a modest AI team runs $500K–$1.5M or more, and the risks are unforgiving: talent attrition can collapse years of institutional knowledge overnight, scope creep is endemic, and realistic times-to-value run 12 to 24 months.

The reward, when executed well, is genuine differentiation – proprietary models trained on institutional data, governance logic you fully own, and a technology moat competitors cannot simply license.

What to buy?

Buying off-the-shelf offers speed, typically one to three months to deployment but introduces fragile integrations, hidden compliance gaps, and vendor lock-in that compounds quietly over time.

The smarter version of “buy” is the strategic middle ground: acquiring talent through M&A or co-building with specialized partners. This path succeeds at twice the rate of internal builds, because external partners bring cross-industry pattern recognition that internal teams rarely develop on their own. The critical caveat: IP ownership and structured knowledge transfer must be non-negotiable terms from day one, not afterthoughts.

Agentic AI is the forcing function that makes this decision permanent. Unlike conventional software, autonomous agents are designed to plan, decide, and execute independently and in doing so, they weave themselves into the fabric of an institution’s core financial cycles. The enduring cost is no longer just maintaining code. It is maintaining institutional trust, audit trails, access controls, and complex data lineage across systems that never stop running.

Once an agentic system has been operational for 12 to 24 months, it accumulates invisible obligations, specialized configurations, model adjustments, regulatory dependencies – that make extraction functionally impossible without massive operational disruption. By the time an organization recognizes a platform choice was sub-optimal, the window to act has already closed.

This is what makes 2026 categorically different from prior technology inflection points. The decision is not a phase of digital transformation that can be revisited. It is the establishment of a permanent foundation.

In the age of autonomous agents, your first move is effectively your final move – dictating the structural integrity and competitive agility of your organization for years to come.

Why Are Leading Fintech Incumbents Choosing to Build In-House Again

A growing number of established financial firms are now opting to build their own technology, acknowledging the complexities but driven by the high cost of outsourcing strategic functions to vendors.

This shift is motivated by the desire for greater control over data ownership and regulatory compliance, the need to build a stronger competitive moat, and accumulated frustration with vendors whose solutions often fall short of expectations, being both over-promised and under-delivered.

03 layers in particular are emerging as non-negotiable build candidates:

Building technology internally comes with significant, often underestimated, costs. The scarcity and high price of skilled AI professionals are major hurdles. Development timelines frequently go over schedule, and there is a constant danger of simply duplicating a solution that a specialized vendor has already perfected.

Furthermore, a structural shift is intensifying the pressure on the build vs. buy decision for fintech: the shrinking pool of new fintech startups. With less funding going into early-stage fintechs, the number of reliable vendor partners is decreasing.

Consequently, established companies are increasingly compelled to integrate and adapt general AI infrastructure — originally designed for other sectors — on their own.

The “Buy” Challenge: A Narrowing Innovation Pipeline

For those looking to buy rather than build, the market has fundamentally changed character. The early-stage vendor ecosystem – the fertile ground of seed-funded experiments that once offered incumbents a rich menu of partnership and acquisition options – has dramatically contracted.

The data is stark. In insurtech, deal counts fell 28% year-over-year in 2024, reaching their lowest annual total since 2016. The number of investors making five or more equity insurtech investments collapsed from 57 in 2021 to just 7 in 2024. CB Insights’ State of Insurtech 2024 report captures this contraction clearly: only 113 investors made at least two equity insurtech investments during the year – a 72% drop from the high of 406 investors in 2021.

The geographic dimension matters too. The share of global insurtech funding going to Silicon Valley-based startups dropped from 20% in 2023 to 10% in 2024 – a signal that the world’s most innovation-dense ecosystem is directing its energy elsewhere.

This does not mean buying is the wrong strategy. It means that buyers must be more disciplined than ever.

The risk of over-relying on “buy” is not just vendor lock-in – it is acquiring a vendor incapable of operationalizing their own technology, leaving the institution worse off than if it had never started the engagement.

The difference between a vendor’s polished demo environment and your production environment is precisely where most digital transformations fail.

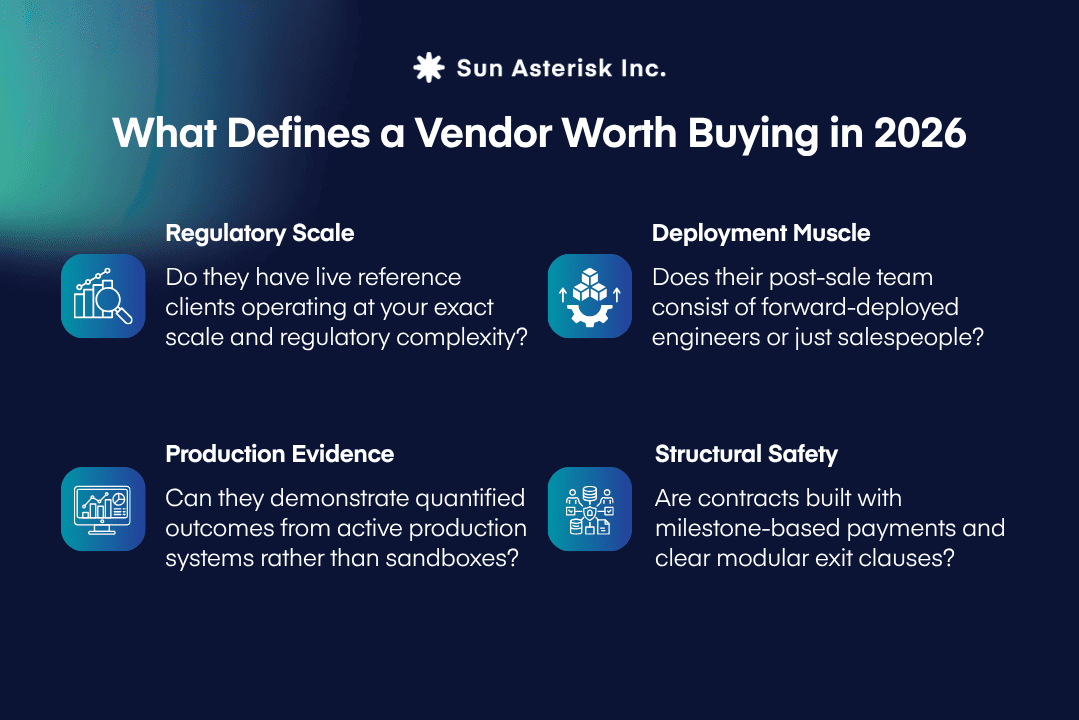

A rigorous buyer’s checklist for 2026 should include at minimum:

What Makes a Technology Partner Actually Reliable in 2026?

The tolerance for speculative partnerships has effectively reached zero. With 95% of enterprise AI investments historically failing to produce measurable ROI, the baseline expectation in 2026 is unambiguous: proven commercial momentum, measurable revenue acceleration, and a technology partner who leads with business outcomes rather than product capabilities. Any partner who opens with a tool demo before asking about your desired outcome is signaling, loudly, that they are not the right fit.

Look at the team

The most telling indicator of a partner’s readiness is not their product – it is who shows up after the contract is signed. Successful AI deployments are built on collaborative execution models where forward-deployed engineers embed with client teams and structured knowledge transfer is part of the engagement from day one. The most common failure pattern is a partner whose pre-sales architects disappear after signature, replaced by a delivery team that inherits a commitment they never made.

The deeper risk is the pilot-to-production chasm. Research suggests 90% of enterprises successfully launch AI pilots, yet enterprise-grade conversion remains the exception. Demos are optimized for clean data and best-case scenarios. Your production environment is neither. That gap is precisely where transformation programs go to die.

Before committing, three questions are non-negotiable:

- Does the partner have reference clients at comparable scale and regulatory complexity?

- Are the people architecting the solution the same ones accountable for delivering it?

- Can they demonstrate quantified outcomes from production systems – not pilots?

Three Contract Terms That Reduce Partnership Risk

Getting the partnership terms right matters as much as choosing the right partner. Milestone-based payments align incentives with your outcomes rather than your partner’s billing cycle.

Explicit exit ramps covering data extraction and transition support are not a sign of distrust – under frameworks like DORA, they are a compliance requirement. And modular, API-first architecture ensures your core data and workflows remain yours regardless of how the partnership evolves.

How LLMs Are Reshaping Financial Product Discovery in 2026

Whether you build or buy, one upstream shift applies universally — and most financial institutions are not yet accounting for it in their build vs. buy decision for fintech technology strategy.

A new technical standard called the Model Context Protocol (MCP) is reshaping how financial products are discovered, recommended, and sold.

Introduced by Anthropic in late 2024 and now governed under the Linux Foundation with backing from Google, Microsoft, AWS, and Bloomberg, MCP is the infrastructure layer that allows AI agents to connect seamlessly to internal data systems and product catalogs through a single standardized protocol. It has moved from experiment to foundational infrastructure in under a year.

But we are entering an era where the search bar is being replaced by the agentic recommendation. A customer no longer types “best home loan rates” into a browser. Instead, their AI-powered personal financial assistant queries available products on their behalf, compares them against the customer’s financial profile, and surfaces a ranked recommendation without the customer ever opening a comparison site.

If your loans, insurance products, or savings accounts are not structured and tagged in a format these agents can parse, you do not appear in that recommendation. You are not losing on price or product quality. You are simply invisible. Personal lines and small commercial segments face the most immediate exposure.

Build vs. Buy for Distribution

If you are building, own the AI layer that touches your highest-value customers directly. The conversational interface, the recommendation logic, the personalization engine — ceding these to a third-party aggregator means ceding the customer relationship itself. For institutions making the build vs. buy decision for fintech, this is the layer where building is non-negotiable.

If you are buying, prioritize the connective tissue — the APIs, embedding platforms, and MCP-compatible data infrastructure that plug your products into the agents your customers already use. Your car insurance surfacing inside a vehicle’s financial OS. Your loan offer triggered by an AI detecting an upcoming large purchase. You do not need to own the agent. You need to be reachable by it.

The institution that wins the distribution layer will not necessarily have the best product. It will have products most legible to the machines making recommendations on their customers’ behalf.

The Decision Framework: Which Layer Do You Own?

The central insight of 2026 is that “build or buy” is the wrong question at the enterprise level. The right question is: which layers must you own, and which can you delegate? No institution can build everything, and no institution can safely buy everything. The answer requires a disciplined mapping of your technology stack to strategic differentiation.

A practical decision matrix helps frame the choices:

| Low Strategic Differentiation | High Strategic Differentiation | High Strategic Differentiation |

| Commodity / Stable | Buy: off-the-shelf; compete on cost and speed of integration | Build: to protect the moat; proprietary advantage requires internal ownership |

| Fast-moving / Agentic | Buy + Integrate Fast: before the market consolidates around a winner | Buy to Build — acquire and deeply customize; speed to differentiation requires external starting point |

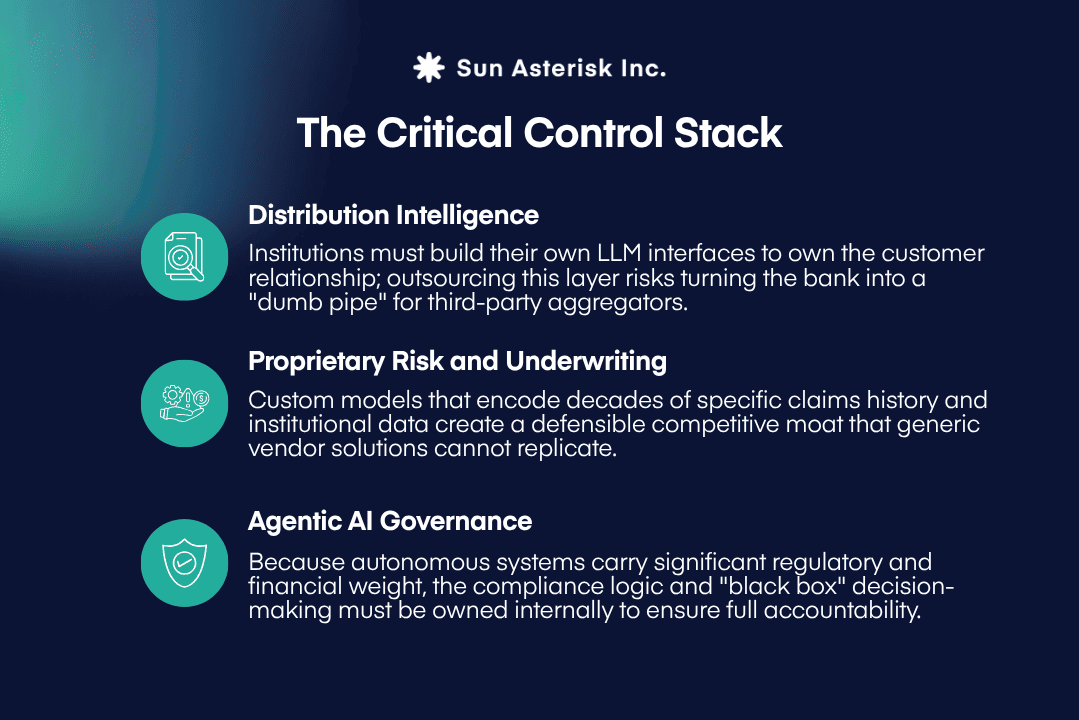

Applied to the full technology stack, this yields a practical three-tier ownership model:

Layer 1: Buy (Commodity)

Outsource: KYC/AML, cloud infra, payments, basic reporting, identity verification. These are commoditized; building is an opportunity cost.

Layer 2: Buy Deep (Operational)

Procure & Integrate: Claims automation, underwriting tools, CRM, CDPs. Vendor provides the foundation; your deep integration and proprietary data provide differentiation.

Layer 3: Build (Differentiation)

Own: Distribution AI/LLM interfaces, proprietary risk models, agentic compliance logic, customer data architecture. These build competitive moats and cannot be outsourced.

How to Evaluate a Vendor Before You Commit

Market indicators offer valuable insight into a vendor’s quality, complementing the primary decision framework. A key signal is their hiring trend, specifically the growth in roles dedicated to implementation, such as forward-deployed engineers and client success architects.

This growth suggests the vendor is truly equipped to deploy, rather than just sell.

For a quantitative assessment, Vendor Mosaic scores – which synthesize financial stability, market momentum, talent acquisition, and customer feedback – provide a concise measure.

Ultimately, the most concrete evidence of capability is their partnership network density: the volume of active, named enterprise-level deployments they manage at a scale comparable to yours.

Consider between Build or Buy in fintech?

Scaling an internal AI team takes time and budget you may not have. Sun*’s dedicated teams plug directly into your setup – bringing instant fintech expertise, reducing hiring costs, and accelerating delivery without losing control of your roadmap.